SEQ Market Update: Cotality Data Confirms East Coast Divergence

While the media focuses heavily on macro-economic headwinds following the RBA’s May move to a 4.35% cash rate, Cotality’s latest Home Value Index shows a sharply uneven market across Australia.

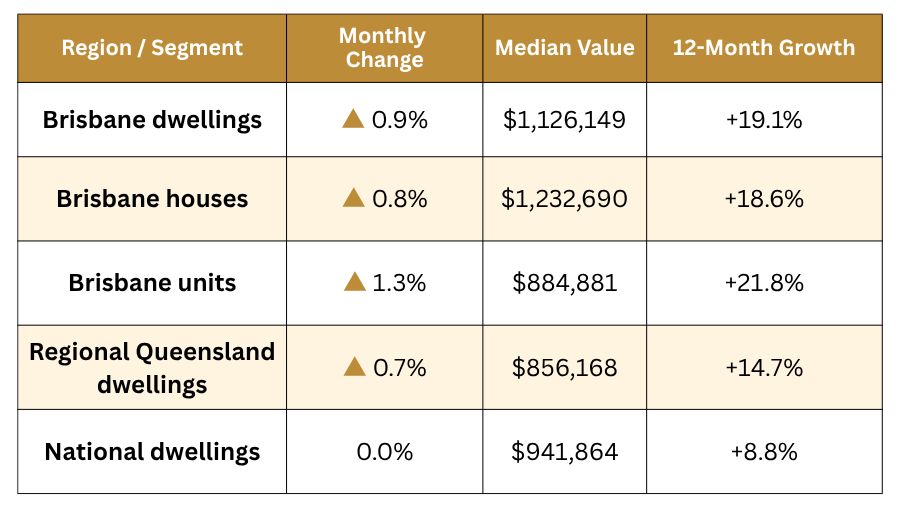

National dwelling values were flat in May, while Sydney and Melbourne moved further into negative territory, falling 0.9% and 0.8% respectively over the month. Brisbane, however, continued to outperform, with dwelling values rising 0.9% in May and 19.1% over the past 12 months.

May 2026 Cotality Performance Index

Affordability constraints are now reshaping demand across South East Queensland. While higher borrowing costs are narrowing the buyer pool, Brisbane’s lower-priced segments remain comparatively resilient. Units are outperforming houses, with Brisbane unit values up 1.3% over the month and 21.8% annually, compared with houses up 0.8% monthly and 18.6% annually.

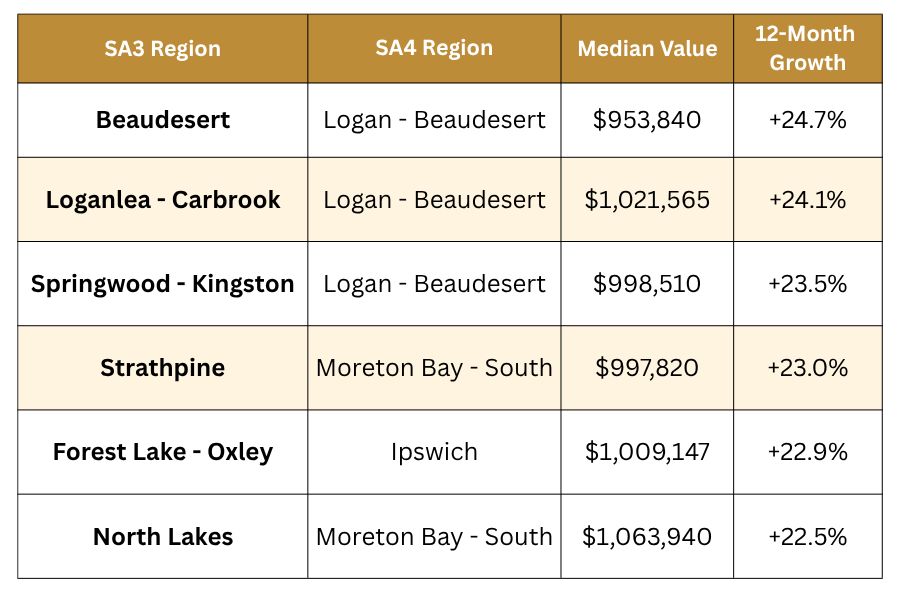

Top Greater Brisbane Growth Corridors

Cotality’s strongest Greater Brisbane growth corridors remain concentrated in the more affordable outer and middle-ring markets. The top-performing regions based on 12-month growth include:

Core Market Fundamentals Driving SEQ Performance

The property research team at Vision Property Buyers has broken down the three core structural pillars keeping the local market insulated:

Structural Supply Deficit: New housing supply remains constrained, with elevated construction costs and feasibility challenges limiting the prospect of a sustained uplift in completions. This continues to place a floor under well-located SEQ markets, even as buyer demand becomes more selective.

Affordability-Led Demand: Brisbane’s median dwelling value has now reached $1.126 million, but relative affordability compared with Sydney continues to support interstate and local upgrade demand. Within Brisbane, this is increasingly pushing buyers toward units, townhouses, and outer-ring growth corridors.

Rental Market Support: Cotality reported national vacancy at 1.5% in May, with rental pressure still elevated. Brisbane’s gross dwelling yield sits at 3.3%, while Regional Queensland is stronger at 4.1%, helping investors offset some of the pressure from higher borrowing costs.

Strategic Outlook

The May data points to a more cautious market, not a uniform correction. Cotality expects momentum to keep easing as affordability, higher rates, and softer sentiment weigh on demand, but conditions are likely to remain uneven across regions and price points.

For South East Queensland, the opportunity is becoming more selective. Broad market momentum is slowing, but well-chosen assets in supply-constrained, infrastructure-supported, and affordability-driven corridors continue to show resilience.

To analyze how these micro-market fundamentals apply to your specific portfolio goals or target suburbs, please contact our team today.

Disclaimer: Home Value Index results are as of 31 May 2026. We recommend that you seek independent financial and taxation advice before acting on any information in this email. It contains general information only and has been prepared without taking into account your objectives, financial situation or needs. We recommend that you consider whether it is appropriate for your circumstances. Your full financial situation will need to be reviewed prior to acceptance of any offer or product.